THE SELF-FUNDING COPPER RE-RATE HIDING IN CHILE’S COASTAL CORDILLERA

Disseminated on behalf of

Red Metal Resources Ltd.

THE SELF-FUNDING COPPER RE-RATE IN CHILIE’S COASTAL CORDILLERA

RED METAL RESOURCES LTD

CSE: RMES | OTC: RMESF

This communication is not an offer to buy or sell securities nor is it to be construed as personal investment advice. Nothing contained in this communication should be relied upon as a promise or representation as to future performance.

FORWARD: COPPER IS NO LONGER AN INDUSTRIAL METAL

Copper is no longer just an industrial metal. It is the wiring behind electrification, the backbone of the grid buildout, the hidden hardware behind AI data centres, the critical input for renewable power, EV infrastructure, defense manufacturing, and every serious attempt to modernize the energy system.

The problem is simple: the world needs more copper, but new copper supply is slow, expensive, political, and increasingly difficult to permit. That creates a rare environment where small, high-grade, infrastructure-backed copper projects in proven mining jurisdictions can become far more important than the market currently appreciates.

That is where Red Metal Resources Ltd (CSE: RMES | OTC: RMESF) enters the picture.

Red Metal is not trying to sell investors on a vague, early-stage land package. The company controls the Carrizal Copper-Gold-Cobalt Property in Chile’s Atacama Region – a historic mining district with high-grade copper pedigree, existing workings, strong infrastructure, and more than 9,000 metres of drilling already completed on the property..

The reason the story has become far more interesting now is that Red Metal has moved beyond being a conventional junior explorer.

In May 2026, the company signed a 5-year renewable mining lease with Minera KMT SpA, a local small-scale Chilean miner, to restart production on the Farellon 1/8 concession. KMT is responsible for mining costs, equipment, labour, development, rehabilitation and annual taxes. Red Metal, through its Chilean subsidiary, retains a royalty-style revenue stream on ore sales and receives ongoing geological information from underground work.

In practical terms, this has the potential to give Red Metal something most juniors do not have: a recurring source of cash flow to help fund exploration, reduce dilution risk, and keep the market engaged with steady operational updates.

For me, this is the key.

Red Metal Resources Ltd (CSE: RMES | OTC: RMESF) is a small-cap copper story with a real asset, a real jurisdiction, a real operating partner, near-term field work, and a potential funding model that is materially different from the usual junior mining treadmill.

The market has not fully priced that shift in yet.

THE CORE THESIS

Red Metal Resources offers investors a high-torque copper opportunity built around five core pillars:

- A 100%-owned copper-gold-cobalt project in Chile’s Coastal Cordillera, one of the world’s most important copper regions.

- A historic high-grade mining district with past production, extensive surface mineralization, and established infrastructure.

- A newly signed renewable mining lease that could create recurring royalty revenue without Red Metal directly funding the mining operation.

- A mature exploration database that includes more than 9,000 meters of drilling, new LiDAR and surface sampling developed targets, and a 37 line-kilometer IP survey designed to sharpen the next drill program.

- A deeply discounted micro-cap valuation that could re-rate quickly if the market begins to price production visibility, exploration success, and improving copper sentiment.

The setup is not complicated.

Red Metal has a small valuation, a real copper asset, a new cash-flow mechanism, and multiple near-term catalysts.

That combination is rare in the junior mining market.

COMPANY OVERVIEW

Red Metal Resources Ltd (CSE: RMES | OTC: RMESF) is a Canadian-listed mineral exploration company focused on copper-gold-cobalt assets in Chile, with additional strategic mineral exposure in Canada.

The company’s flagship asset is the Carrizal Property in Chile’s Atacama Region, located in the Coastal Cordillera – a historically productive and infrastructure-rich copper belt.

Carrizal consists of 21 mining concessions totaling 3,278 hectares and is divided into two project areas: Farellon in the south and Perth in the north. The property sits near the historic Carrizal Alto mining district, which operated during the 1800s and was historically known for high-grade copper production.

Importantly, Carrizal is not a remote, theoretical exploration concept. It benefits from year-round access, proximity to roads, power, water, ports, Vallenar, Copiapo, and a mining-educated workforce.

That infrastructure advantage matters.

In mining, geology creates the opportunity, but infrastructure determines whether that opportunity can realistically advance. Red Metal has both: a high-grade IOCG-style system in a proven district and the local access required to move quickly.

THE TRANSFORMATIONAL CATALYST: THE FARELLON MINING LEASE

The May 2026 mining lease is the event that changed the Red Metal story.

Red Metal’s wholly owned Chilean subsidiary, Minera Polymet SpA, leased the mining rights for the Farellon 1/8 mineral concession to Minera KMT SpA, an experienced local small-scale miner.

The agreement is structured as a 5-year renewable mining lease. After a 7-month development period, KMT must maintain minimum monthly production of 2,500 tonnes of ore to keep the agreement in good standing.

The royalty-style economics are important:

- Red Metal’s Chilean subsidiary receives 10% on copper, silver and gold ore sales, less an existing 1.5% royalty – effectively about 8.5% net.

- For cobalt-bearing ore, if sold, the subsidiary receives 15% less the existing 1.5% royalty – effectively about 13.5% net.

- KMT is responsible for mining costs, equipment, labour, rehabilitation, development work and annual taxes on the concession.

- Red Metal gains revenue exposure without taking on direct operating cost risk at the mine level.

This matters because junior mining investors are used to one thing: dilution.

A company raises money, drills, waits for results, runs low on cash, and raises again – often at lower prices. Red Metal is attempting to break that cycle by pairing exploration upside with a recurring revenue stream from historic high-grade workings.

According to management estimates referenced in the draft materials, steady-state royalty revenue could potentially reach approximately CAD $50,000 to CAD $80,000 per month once production is established. That is not guaranteed, and it remains dependent on production rates, grades, recoveries, metal prices, and ramp-up execution.

But if achieved, it could be a major differentiator for a company currently trading at a micro-cap valuation.

For investors, the lease potentially does three things at once:

- It reduces funding pressure

- It validates the near-term mining potential of Farellon, and

- It Creates a steady stream of operational updates that can keep the market engaged.

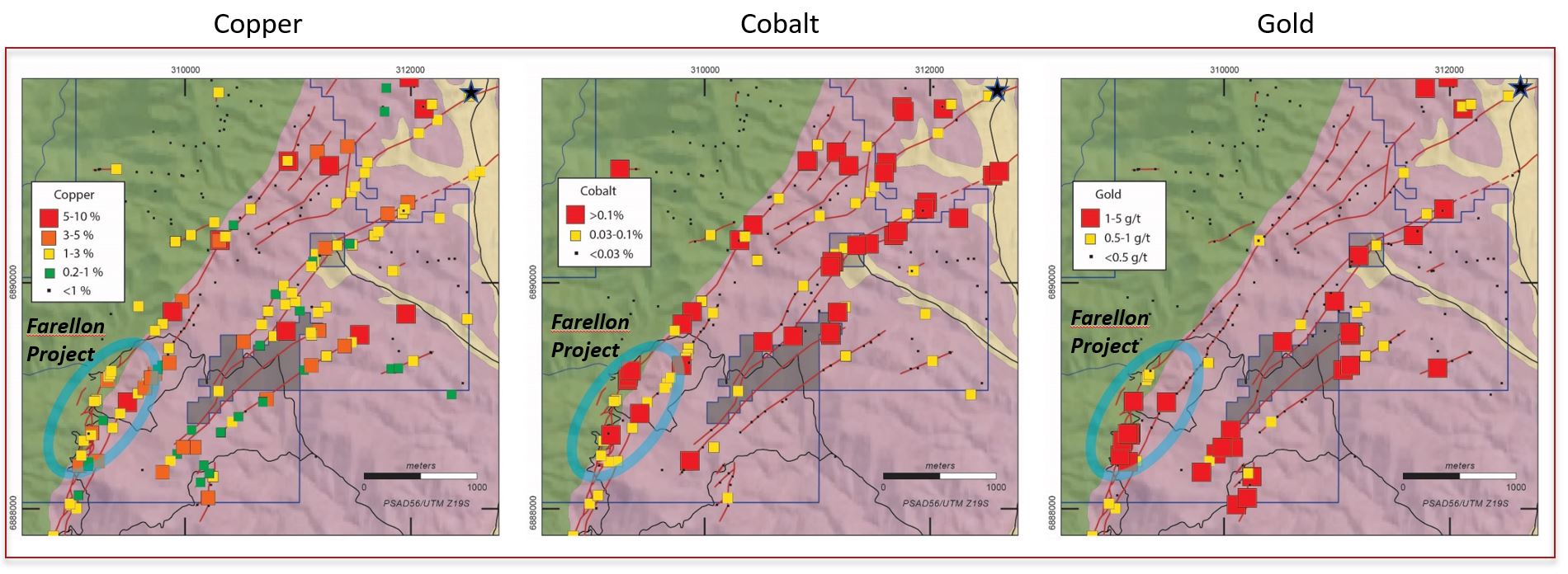

WHY FARELLON MATTERS

Farellon is the core engine of the Carrizal story.

The project is an IOCG-style vein system located along a major northeast-trending fault zone. Mineralization is hosted in quartz-calcite veins containing chalcopyrite, bornite and chalcocite, with vein widths historically described in the 3–6 metre range and lower-grade mineralized halos extending beyond the veins.

The property already has meaningful technical work behind it.

Farellon has seen more than 9,000 metres of drilling between 1996 and 2022. Drilling has verified approximately 1.5 kilometres of mineralized strike length, with the system open for an additional estimated 3.5 kilometres along strike and open at depth.

In 2022, drilling also intersected a parallel structure known as the Gorda Vein at depth, adding another layer of exploration potential.

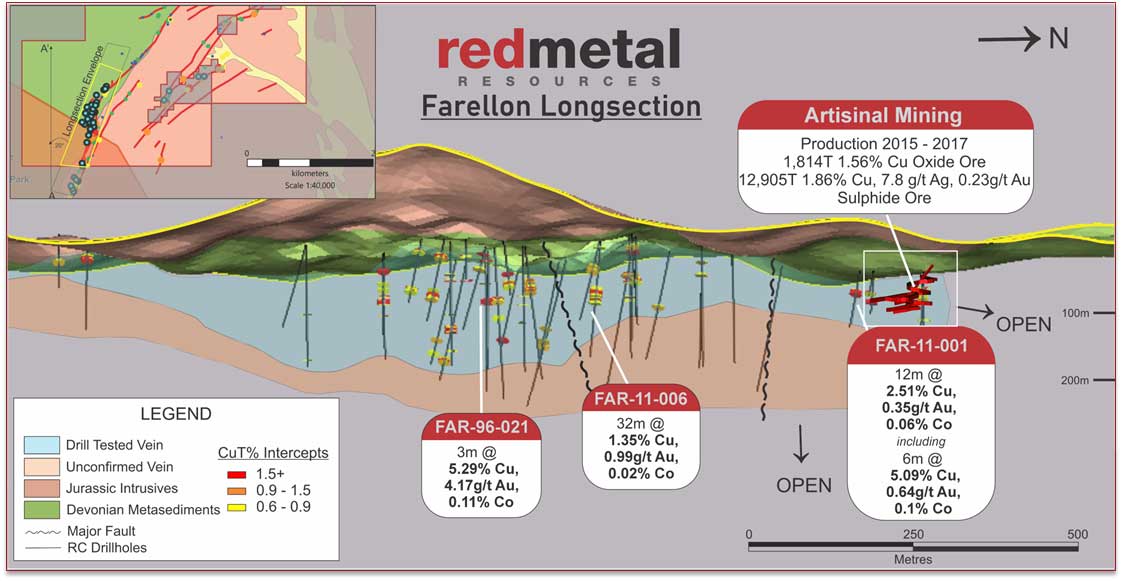

The historical mining data adds important context.

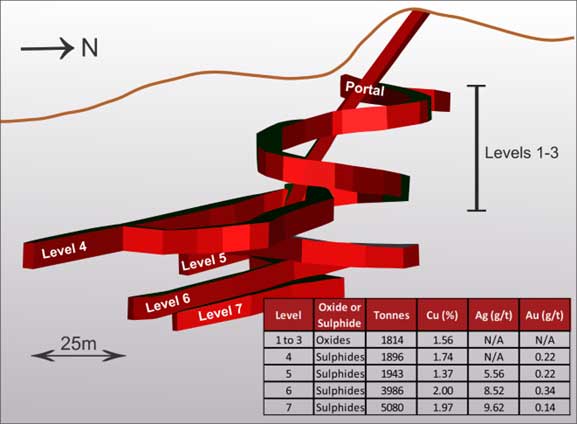

Between 2015 and 2017, mining activities at Carrizal produced 12,905 tonnes of sulphide ore transported to ENAMI, containing 528,168 pounds of copper, 2,829 ounces of silver and 95 ounces of gold.

The company also reported that Level 7 alone produced 5,080 tonnes between 2016 and 2017 at 1.97% copper, 9.62 g/t silver and 0.14 g/t gold.

Those historical numbers do not guarantee future production. But they do show why the company and its local mining partner are focused on rehabilitating historic workings and restarting activity in known mineralized zones.

This is not a blind bet. It is a high-grade copper system with known underground development, past production, new geophysics, and room to expand.

LIDAR + IP: TURNING HISTORIC WORKINGS INTO MODERN TARGETS

One of the strongest parts of the Red Metal Resources Ltd (CSE: RMES | OTC: RMESF) setup is that the company is not relying on old data alone.

It is layering modern exploration tools over a historic mining district.

In April 2026, Red Metal reported that detailed LiDAR analysis had confirmed previously identified mineralized vein structures and extended their limits in both directions. The work outlined several new zones with parallel structures near documented mineralized veins and identified numerous historic excavation pits, which may indicate additional mineralized structures.

The LiDAR work highlighted four areas of dense historic artisanal workings with little or no previous surface sampling, outlined 30 veins, and identified four new target areas based on structural interpretation and the density of historic workings.

That is exactly the kind of data that can convert a historical district into a modern exploration story.

Red Metal also commenced a 37 line-kilometer induced polarization survey at Carrizal. The IP survey is designed to detect chargeability associated with sulphide mineralization and evaluate targets down to approximately 500 meters depth.

The company has stated that the combined LiDAR interpretation, surface sampling and IP data will be incorporated into high-confidence drill targets.

That is the next major exploration arc: historic high-grade district + modern geophysics + drill targeting.

The market generally rewards juniors when a story moves from concept to target generation to drilling, especially when the broader commodity backdrop is supportive.

THE CHILEAN ADVANTAGE

Chile is the world’s copper heavyweight.

But Red Metal’s advantage is more specific than simply being in Chile. The company is positioned in the Coastal Cordillera, a lower-elevation belt with better access, proximity to infrastructure, proximity to ports, and a long history of mining activity.

This is an important distinction.

Much of Chile’s modern copper development has focused on large-scale, lower-grade porphyry systems in the high Andes. Those deposits can be massive, but they are also capital intensive, technically complex, and often slow to permit and develop.

Coastal Cordillera projects can offer a different profile: smaller, higher-grade, infrastructure-backed deposits that may be advanced more quickly, especially through Chile’s well-developed small-scale mining framework.

Red Metal Resources Ltd (CSE: RMES | OTC: RMESF) fits that lane.

The company is not trying to build a mega-mine from scratch. It is working in a historic district with existing underground development, local mining expertise, and a structure that could generate revenue while exploration advances.

In today’s copper market, speed and grade matter.

COPPER MACRO: THE METAL THE WORLD CANNOT BUILD WITHOUT

The macro backdrop is exactly why Red Metal Resources Ltd (CSE: RMES | OTC: RMESF) deserves attention now.

Copper demand is being pulled by several long-duration themes at the same time: electrification, transmission infrastructure, renewable power, EVs, industrial reshoring, AI data centres, defense spending, robotics, and grid hardening.

The challenge is that copper supply does not respond quickly.

New mines often take years – and sometimes decades – to permit, finance, build and commission. Existing mines are facing declining grades, rising capital intensity, and growing political and social-license pressure.

The result is a market where even modest new sources of copper become increasingly valuable.

This is the bigger-picture investment case.

Red Metal does not need to become a global copper giant to create value from its current valuation. It needs to execute: ramp the mining lease, demonstrate recurring revenue, refine targets, drill intelligently, and continue proving that Carrizal has district-scale potential.

In a structurally tight copper market, that could be enough to force a meaningful re-rate.

VALUATION: THE DISCONNECT IS THE OPPORTUNITY

Red Metal Resources Ltd (CSE: RMES | OTC: RMESF) currently trades like a forgotten micro-cap explorer, despite now having a new production-linked royalty structure, a mature exploration dataset, new geophysical targeting, historical production, and exposure to one of the strongest long-term commodity themes in the market.

With approximately 56.84 million shares outstanding and a recent quote near ~CAD $0.10, the company’s basic market capitalization is roughly ~CAD $5.5 million.

That is the entire valuation being placed on Carrizal, the Farellon mining lease, Perth, the Quebec hydrogen optionality, Ontario exposure, the drilling database, and the next round of exploration catalysts.

That creates a clear asymmetry.

If Red Metal proves that the mining lease can generate consistent monthly royalty revenue, the company may no longer be valued as a conventional early-stage explorer.

If IP results define compelling sulphide targets and drilling confirms extensions or parallel zones, the market could begin valuing Red Metal as a catalyst-rich copper exploration and royalty-backed development story.

An illustrative CAD $25 million to CAD $40 million valuation would represent roughly a 4x to 7x move from a CAD $5.7 million starting point.

A stronger discovery or resource-definition scenario could justify a materially higher valuation, particularly in a rising copper market.

These are not price targets. They are valuation scenarios showing how powerful the re-rate could be if execution lines up.

ADDITIONAL UPDISE: PERTH, QUEBEC HYDROGEN AND ONTARIO

The flagship story is Carrizal, and the market should value Red Metal primarily on Carrizal execution. But the company also carries additional optionality that could matter over time.

The Perth project, also part of Carrizal, adds further copper-gold-cobalt vein potential north of Farellon. Historical work has identified multiple high-grade vein targets and a broad surface geochemistry database.

If Farellon gains traction, Perth becomes a logical second layer of district-scale upside.

In Canada, Red Metal also holds 100%-owned Ville Marie claims in Quebec’s emerging natural hydrogen district, as well as Larder Lake claims in Ontario.

This Canadian portfolio should be viewed as optional upside rather than the core reason to own the stock. But in a market where clean energy and strategic minerals continue to attract capital, it gives Red Metal another angle beyond Chilean copper.

NEAR-TERM CATALYSTS

The reason Red Metal Resources Ltd (CSE: RMES | OTC: RMESF) is timely is that the story has a stacked catalyst profile.

This is not a company waiting years for something to happen. The next 6–12 months could bring multiple developments that help the market reassess the valuation:

- Mining lease ramp-up: KMT development work and progress toward the minimum 2,500 tonnes per month production requirement after the development period.

- Royalty revenue visibility: early evidence of recurring revenue from ore sales could materially change the market’s perception of the company.

- Underground data flow: production and development work should provide additional geological information from known mineralized zones.

- IP survey results: 37 line-kilometres of IP designed to identify chargeability anomalies associated with sulphide mineralization to roughly 500 metres depth.

- Drill planning and potential drilling: LiDAR, IP and surface sampling data will be combined to generate high-confidence drill targets.

- Farellon expansion potential: follow-up work on known strike extensions, depth extensions, and parallel structures including the Gorda Vein.

- Sector rotation: stronger copper prices, AI power demand, grid investment, and resource nationalism could bring capital back into small-cap copper names.

- Market awareness: recent treasury strengthening and investor awareness initiatives could increase visibility in a stock that has historically traded below its asset potential.

RISKS & MITIGANTS

Red Metal Resources Ltd (CSE: RMES | OTC: RMESF) is still a junior mining company, and junior mining carries meaningful risk. The upside is high because the valuation is low, but investors need to understand the risk profile.

Production ramp-up risk: KMT must rehabilitate and develop historic workings before consistent production is achieved. The experienced local operator and known Level 7 mineralization help reduce, but do not eliminate, this risk.

Grade and tonnage variability: Historical production shows copper, silver and gold content, but future results can vary materially. Ongoing production data will be important.

No current mineral resource: Red Metal has extensive drilling and historical work, but no current NI 43-101 resource has been defined at Farellon. Future drilling is required to advance resource confidence.

Commodity price volatility: Copper, gold, silver and cobalt prices can move sharply. High-grade potential and by-product credits may help, but metal prices remain outside company control.

Funding and dilution risk: The mining lease could reduce future equity funding needs if royalty revenue develops as expected. However, aggressive exploration may still require additional capital.

Liquidity risk: RMES remains a micro-cap issuer with limited trading liquidity. Increased awareness can help, but liquidity should not be assumed.

Jurisdiction and operational risk: Chile is a world-class copper jurisdiction, but permitting, taxes, labour, local execution and mining regulations still matter.

CONCLUSION – WHY RED METAL, WHY NOW

Red Metal Resources Ltd (CSE: RMES | OTC: RMESF) has reached the type of inflection point that junior mining investors look for before the broader market catches on.

The company has a real copper-gold-cobalt asset in Chile’s copper heartland. It has a historic high-grade district, strong infrastructure, existing underground workings, more than 9,000 metres of drilling, modern LiDAR-defined targets, an active IP survey, and a planned path toward drilling.

Most importantly, it now has a 5-year renewable mining lease that could generate recurring royalty revenue while shifting mining costs to an experienced local operator.

That is the differentiator.

Red Metal is no longer just asking investors to fund exploration and wait. It is attempting to build a self-funding copper model where production-linked revenue supports exploration, exploration supports discovery potential, and each new data point gives the market another reason to re-rate the story.

At roughly a CAD $5–6 million market capitalization, the market is still treating Red Metal as if nothing has changed.

But something has changed.

The company has moved from passive exploration to an active, catalyst-rich phase with cash-flow potential, modern targeting, and exposure to one of the most important metals in the global economy.

Copper is entering a long-cycle supply problem. The world needs new copper. Chile remains one of the best places on earth to find and develop it. Red Metal controls a high-grade project in a historic district, and the next chapter is already underway.

For investors looking for asymmetric copper exposure, Red Metal Resources Ltd (CSE: RMES | OTC: RMESF) is exactly the kind of small-cap story that deserves attention before the execution becomes obvious.

THE BOTTOM LINE

Red Metal Resources Ltd (CSE: RMES | OTC: RMESF) is a micro-cap copper story with a rare combination: historic high-grade production, modern exploration catalysts, Chilean infrastructure, potential royalty cash flow, and a valuation that still looks disconnected from the opportunity.

If the mining lease performs and drilling begins to validate the broader system, this is the type of stock that can move before the broader market fully understands why.

Stay up to date with Spartan’s Weekly Newsletter

This communication is for informational purposes only and should not be construed as an offer to buy or sell securities nor is it to be construed as personal investment advice. Nothing contained in this communication should be relied upon as a promise or representation as to future performance. An affiliate of Spartan Trading Inc. (“Spartan”) has been engaged by Red Metal Resourced Ltd (RE) to provide it with consulting, promotional and or marketing services, and the information contained in this communication has been prepared on behalf of RE. Spartan’s affiliate may receive compensation in the form of cash or securities from time to time for these services and may sell any such securities as permitted by law. Neither the information presented nor any statement or expression of opinion, or any other matter herein, directly or indirectly constitutes a solicitation of the purchase or sale of any securities. Neither the owner of Spartan nor any of its members, officers, directors, contractors or employees are licensed broker-dealers, account representatives, market makers, investment bankers, investment advisers, analyst or underwriters. Investing in securities, including the securities of those companies profiled or discussed on this website is for individuals tolerant of high risks. Viewers should always consult with a licensed securities professional before purchasing or selling any securities of companies profiled or discussed on Spartan Trading Inc related properties. It is possible that a viewer’s entire investment may be lost or impaired due to the speculative nature of the companies profiled. Remember, never invest in any security of a company profiled or discussed on this website unless you can afford to lose your entire investment. Also, investing in micro-cap securities is highly speculative and carries an extremely high degree of risk. Spartan makes no recommendation that the securities of the companies profiled or discussed on this website should be purchased, sold or held by viewers that learn of the profiled companies through our website. Some of the content on this website contains “forward-looking statements.” Such statements may be preceded by the words “intends,” “may,” “will,” “plans,” “expects,” “anticipates,” “projects,” “predicts,” “estimates,” “aims,” “believes,” “hopes,” “potential,” or similar words. Forward-looking statements are not guarantees of future performance, are based on certain assumptions, and are subject to various known and unknown risks and uncertainties, many of which may be beyond a company’s control, and cannot be predicted or quantified, and, consequently, actual results may differ materially from those expressed or implied by such forward-looking statements.

It is hereby noted that forward-looking statements contained herein may include everything other than historical information, involve risk and uncertainties that may affect a company’s actual results of operation. A company’s actual performance could greatly differ from those described in any forward-looking statements or announcements mentioned on this website or the websites contained within. Factors that should be considered that could cause actual results to differ include: the size and growth of the market for the company’s products; the company’s ability to fund its capital requirements in the near term and in the long term; pricing pressures; unforeseen and/or unexpected circumstances in happenings; etc. and the risk factors and other factors set forth in the company’s filings with the Securities and Exchange Commission. However, a company’s past performance does not guarantee future results. Generally, the information regarding a company profiled or discussed on this website is provided from public sources www.spartantrading.com and affiliates makes no representations, warranties, or guarantees as to the accuracy or completeness of the information provided or discussed. Viewers should not rely solely on the information obtained through our website or in communications originating from our website. Viewers should use the information provided by us regarding the profiled companies as a starting point for additional independent research on the companies profiled or discussed in order to allow the viewer to form his or her own opinion regarding investing in the securities of such companies. Factual statements, or the similar, made by the profiled companies are made as of the date stated and are subject to change without notice and Spartan, nor its affiliates, has no obligation to update any of the information provided. Spartan, its owners, officers, directors, contractors and employees are not responsible for errors and omissions. From time to time certain content on this website is written and published by our employees or third parties. In addition to information about our profiled companies, from time to time, our website will contain the symbols of companies and/or news feeds about companies that are not being profiled by us but are merely illustrative of certain activity in the micro cap or penny stock market that we are highlighting.

Viewers are advised that all analysis reports and news feeds are issued solely for informational purposes. Any opinions expressed are subject to change without notice. It is also possible that one or more of the companies discussed or profiled on this website may not have approved certain or any statements within the website. Spartan encourages viewers to supplement the information obtained from this website with independent research and other professional advice. The content on this website is based on sources which we believe to be reliable but is not guaranteed by us as being accurate and does not purport to be a complete statement or summary of the available data. Third Party Web Sites and Other Information This website may provide hyperlinks to third party websites or access to third party content. Spartan, its owners, officers, directors, contractors and employees are not responsible for errors and omissions nor does Spartan control, endorse, or guarantee any content found in such sites. Spartan does not control, endorse, or guarantee content found in such sites. By accessing, viewing, or using the website or communications originating from the website, you agree that Spartan, its owners, officers, directors, contractors and employees, are not responsible for any content, associated links, resources, or services associated with a third party website. You further agree that Spartan, its owners, officers, directors, contractors and employees shall not be liable for any loss or damage of any sort associated with your use of third party content. Links and access to these sites are provided for your convenience only. Spartan uses third parties to disseminate information to subscribers. Although we take precautions to prevent others from obtaining our subscriber list, there is a risk that our subscriber list, through no wrong doing on our part, could end up in the hands of an unauthorized party and that subscribers will receive communications from unauthorized third parties. We encourage viewers to invest carefully and read the investor issuer information available at the web sites of the United States Securities and Exchange Commission (SEC). The SEC has launched an investor-focused website to help you invest wisely and avoid fraud at www.investor.gov and filings made by public companies can be viewed at www.sec.gov and/or the Financial Industry Regulatory Authority (FINRA) at: www.finra.org. In addition, FINRA has published information at its website on how to invest carefully at www.finra.org/Investors/index.htm. Income Disclaimer Testimonials and examples used here are exceptional results which may not apply to the average purchaser. They are not intended to represent or guarantee that anyone will achieve the same or similar results through our service. The use of our information should be based on your own due diligence, and you agree that our company is not liable for any success or failure of your business that is directly or indirectly related to the use of our information. As with any business, your results may vary, and will be based on your individual capacity, business experience and expertise. There are no guarantees concerning the level of success you may experience. Income statements made by our customers are only estimates of what they have earned; there is no guarantee that you will make these levels of income. When using our information you accept the risk that these earnings and income statements differ by individual. There is no assurance that examples of past earnings can be duplicated in the future. There are unknown risks in business and on the internet that we cannot anticipate which can reduce results. We therefore cannot guarantee your future results or success and are not responsible for your actions. Spartan Trading Inc an affiliate of Spark Newswire Inc. has been retained by Spark Newswire Inc. to perform consulting, promotional and or advertising services for a limited time with respect to the company we are profiling or discussing on this website and in exchange for such services Spark Newswire Inc. has received cash compensation from RE (OTCPINK:RMESF). Questions regarding this website may be sent to info@spartantrading.com. Spark Newswire Inc an affiliate of Spartan Trading Inc. has a two month agreement with RE (OTCPINK:RMESF) for the sum of one hundred and twenty five thousand dollars. This agreement is for consulting and or marketing of RE (OTCPINK:RMESF) which services include the issuance of this release and other opinions that we release concerning of RE (OTCPINK:RMESF) and may be renewed from time to time. Spartan Trading an affiliate Spark Newswire Inc has not investigated the background of RE (OTCPINK:RMESF) the hiring party. Anyone viewing this newsletter should assume Spartan or affiliates own shares RE (OTCPINK:RMESF) which they plan to liquidate, and further understand that the liquidation of those shares may or may not negatively impact the share price. Spark Newswire Inc has received this amount as a consulting and or production budget for advertising efforts and will retain amounts over and above the cost of production, copywriting services, mailing and other distribution expenses as a fee for Spark Newswire Inc’s services. As such, our opinion is neither unbiased nor independent, and you should consider that when evaluating our statements RE (OTCPINK:RMESF).

PLEASE READ OUR DISCLAIMER STATEMENT BEFORE VIEWING FOR EDUCATIONAL AND INFORMATION PURPOSES ONLY; NOT INVESTMENT ADVICE. Any Spartan Trading Service offered is for educational and informational purposes only and should NOT be construed as a securities-related offer or solicitation, or be relied upon as personalized investment advice. Results may not be typical and may vary from person to person. Making money trading stocks takes time, dedication, and hard work. There are inherent risks involved with investing in the stock market, including the loss of your investment. Past performance in the market is not indicative of future results. Any investment is at your own risk. Spartan Trading testimonials depicting profitability are believed to be true based on the representations of the persons voluntarily providing the testimonial. However, subscribers’ trading results have NOT been tracked or verified and past performance is not necessarily indicative of future results, and the results presented in this communication are NOT TYPICAL. Actual results will vary widely given a variety of factors such as experience, skill, risk mitigation practices, market dynamics and the amount of capital deployed. Investing in securities is speculative and carries a high degree of risk; you may lose some, all, or possibly more than your original investment. Becoming an experienced trader takes hard work, dedication and a significant amount of time. As a provider of educational courses, we do not have access to the personal trading accounts or brokerage statements of our customers.

I/we have a beneficial long or Short position in the shares of Any Ticker We speak about on Zoom Streaming or in Discord either through stock ownership, options, or other derivatives

Full Disclaimer, Terms & Conditions:

https://spartantrading.com/terms-conditions/